The overall economy continues to improve, with all major economic indicators signaling a trajectory of continuing growth. GDP ended 2014 very strongly, with forecasts calling for 3% growth in 2015. Business confidence reached a level of 61, signaling average belief in expansionary business conditions.

Economic conditions are supporting growth in demand for construction activity, particularly for nonresidential buildings. The nonresidential construction sector is now looking at double-digit increases in 2015, led by vigorous levels of demand for hotels and office buildings.

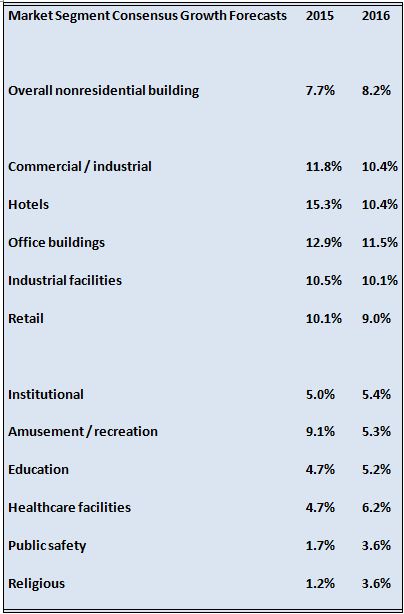

The AIA’s semi-annual Consensus Construction Forecast, a survey of the nation’s leading construction forecasters, projects that nonresidential construction spending increase 7.7% in 2015.

Lighting industry performance in 2014

The National Electrical Manufacturers (NEMA) Lighting Systems Index increased 1.9% from the second to the third quarters of 2014, climbing to its highest level to date in calendar year 2014. The index posted a gain of 4.1% on a year-over-year basis. Shipments of emergency lighting, fixtures, and miniature lamps improved during the quarter; however, ballast and large lamp shipments fell.

NEMA’s shipment index for T12 lamps bested the previous two quarters by advancing 8.6% from the second quarter to the third. In contrast, shipments of T5 and T8 lamps decreased by 6.6% and 11.1%, respectively. All three indexes are in negative territory on a year-over-year basis for 2014 through the third quarter. T12 lamps secured an increase in market share for the quarter posting a gain of 3.2% to reach a share of 22.2%. The share of T5 lamps was unchanged at 10%. Meanwhile, the market share for T8 lamps decreased to 67.8%.

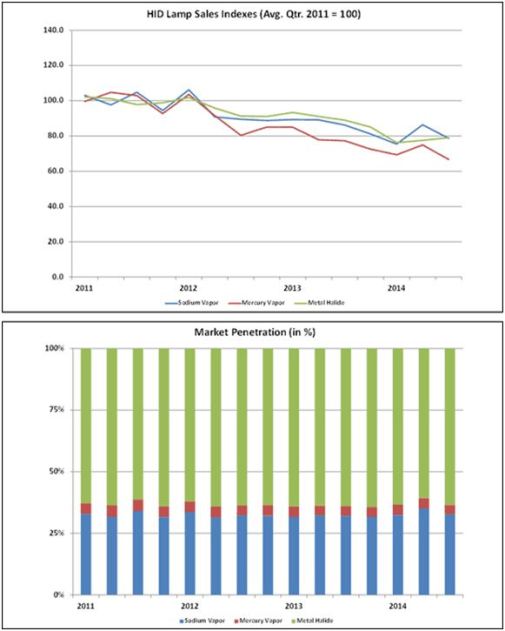

High intensity discharge (HID) lamp shipments, as measured by NEMA’s HID indexes, showed quarterly declines in two of the three lamp types. Sodium- and mercury-vapor lamps slipped 8.9% and 10.9%, respectively, from the second quarter to the third quarter. Only the index for metal halide increased during the quarter, posting a modest gain of 2%. Shipments of metal halide lamps increased 2.7% to a share of 63.5% of the HID market. The market share for sodium vapor lamps slipped to 32.7%, a decline of 2.3 percentage points. Mercury vapor lamps decreased by 0.4 points to a share of 3.8%.

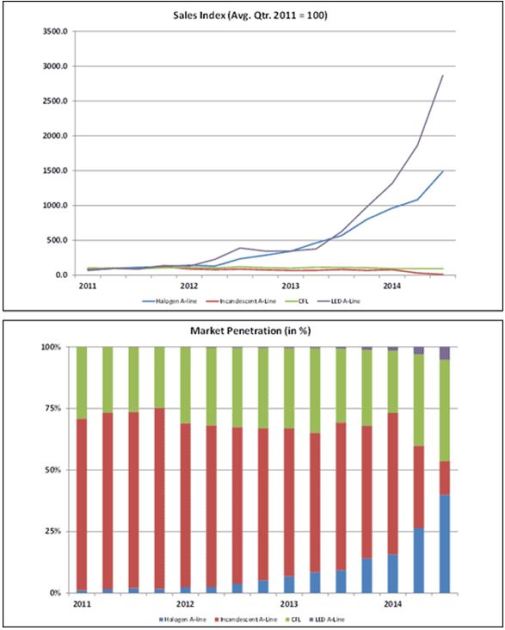

NEMA’s index for compact fluorescent lamp (CFL) shipments registered a year-over-year decline of 14.5% in the third quarter of 2014 despite a modest quarterly increase of 1.5%. For the first three quarters of 2014, the CFL index decreased 13.1% compared to the same period last year. The shipments index for incandescent A-line lamps posted a decline of 62.9% (q/q). In contrast, shipments of LED A-line and halogen A-line lamps continued to grow, showing quarterly gains of 53.8% and 37.7%, respectively. The proliferation of halogen A-line lamp shipments, and subsequent decline in shipments of incandescent A-line lamps, has resulted in an increase in market share for halogen A-line lamps. Halogen A-line lamps captured a share of 39.9% during the quarter, second only to CFLs, which continued to hold a narrow lead with a 41.1% share. The share of LED lamp shipments was 5.1%, an increase of 2 percentage points. Incandescent A-line lamps fell nearly 20 points to a share of 13.6%.

2014 Construction Spending

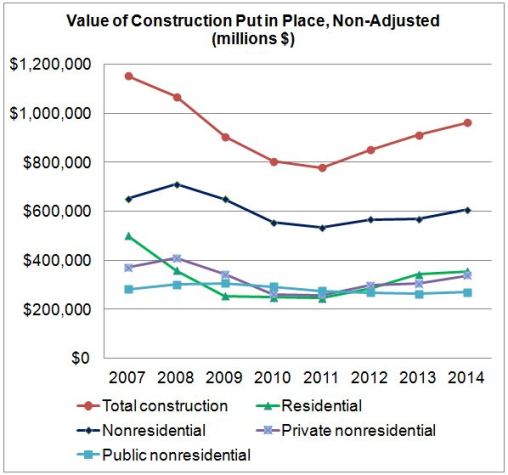

Growth in construction spending in 2014 continued to outpace the U.S. economy. Estimated total put-in-place construction spending—actual numbers, not seasonally adjusted—grew at a healthy 5.6% in 2014. The AIA Consensus Construction Forecast for 2014 had predicted a growth rate of 5.8%.

Based on year-end numbers at the Commerce Department, total put-in-place construction spending reached $961.4 billion in 2014. This rate was slower than previous increases of 7.1% for 2013 and 9.2% for 2012, however.

In 2013, the residential market saw the biggest gains, as a robust market for apartments and single-family houses outweighed downturns in private nonresidential and public projects. In 2014, private nonresidential construction saw the biggest gains, with spending achieving a level of $337 billion, 10.5% increase over 2013. Residential construction was $355.2 billion, a 3.4% increase.

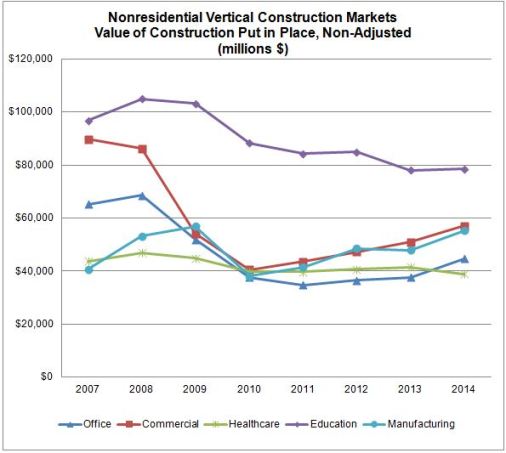

The nonresidential building market was hamstrung by weather-related delays during the first part of the 2014, but conditions improved dramatically throughout the rest of the year to finish with greater than anticipated spending levels. Overall nonresidential construction was $606.2 billion, an increase of 6.6%. Public nonresidential spending was $269.2 billion, a 2.1% increase, demonstrating a modest turnaround after posting a 2% decrease in 2013. Below are five major nonresidential construction markets. All showed increases in total put-in-place construction in 2014 except for healthcare (-6.2%). The office market grew 18.9%, manufacturing 15.1%, commercial 11.9% and education less than 1%.

“For the first time in nearly a decade there was growth in all three major construction segments-public, private nonresidential and residential,” said Ken Simonson, the association’s chief economist. “If the president and Congress can work out a way to pay for long-term investments in our aging infrastructure, there is a good chance this pattern will repeat in 2015.”

Current Construction Indicators

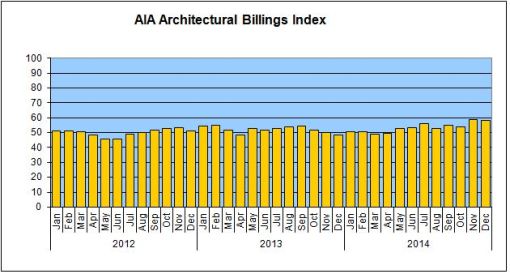

As a leading indicator of construction activity, the American Institute of Architects’ (AIA) Architecture Billing Index, or ABI, reflects the approximate 9- to 12-month lead time between architecture billings and construction spending.

With the exception of March and April, the ABI stayed above 50 throughout the year, indicating an increase in billings and signaling an expansionary market for design services. The year ended on a positive score of 58.2. Regionally, the South (56.8), West (52.9) and Midwest (50.8) has a more optimistic outlook than the Northeast (45.5). The multifamily residential (55.7), institutional (52.5) and commercial/industrial (51.2) indices suggested growth, while the mixed-practice sector rating (45.8) suggests contraction. The new projects inquiry index was 58.2.

“Business conditions continue to be the strongest at architecture firms in the South and the Western regions,” said AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “Particularly encouraging is the continued solid upturn in design activity at institutional firms, since public sector facilities were the last nonresidential building project type to recover from the downturn.”

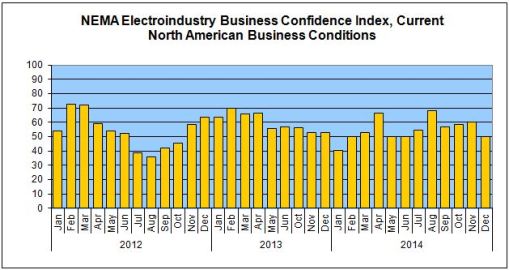

The electrical industry overall expressed optimism about current economic conditions throughout most of 2014.The National Electrical Manufacturers Association’s (NEMA) Electroindustry Business Conditions Index (EBCI) for current conditions in North America stayed at or above a score of 50 for every month except January. The December score was 50, with one-quarter of the panelists reporting conditions improving during the month and the same share reporting they declined. Half the panelists reported no change in conditions between November and December.

December’s EBCI for future North American conditions remained above the 50-point break even mark but retreated to 65. Half of December’s panelists expect the business environment to improve over the next six months compared to 20% who expect it to decline. Thirty percent of panelists expect conditions to remain largely unchanged from the end of 2014 in the first half of 2015.

Meanwhile, 80% of construction firms plan to expand their payrolls in 2015 while only 7% expect to reduce headcounts, according to a survey conducted by the Associated General Contractors of America. The survey, conducted as part of Ready to Hire Again: The 2015 Construction Industry Hiring and Business Outlook, indicates that most contractors are optimistic about the year ahead and ready to expand, but will have to cope with challenges including worker shortages and regulatory burdens.

“Contractors are extremely optimistic about the outlook for 2015,” said Stephen E. Sandherr, the association’s chief executive officer. “Indeed, if their predictions prove true, industry employment could expand this year by the most in a decade.”

AIA Consensus Forecast Predicts Growth for the Nonresidential Construction Market

The AIA’s semi-annual Consensus Construction Forecast, a survey of the nation’s leading construction forecasters, is projecting that spending will see a 7.7% increase in 2015.

“This is the first time since the Great Recession that every major building category is projected to see increases in spending,” said Baker of the AIA. “But by far, the most significant driver that will fuel greater expansion in the marketplace is the revival in the institutional sector, especially with growing demand for new healthcare and education facilities, which alone traditionally account for a third of spending on new building construction.”

The improvement trend is expected to strengthen even further in 2016, with the AIA Consensus Construction Forecast projecting an 8.2% increase in nonresidential construction spending.

Source: AIA Consensus Construction Forecast, calculated as an average of all forecasts provided by the panelists that submit forecasts for each of the above building categories: McGraw-Hill Construction, IHS-Global Insight, Moody’s Economy.com, FMI, Reed’s Construction Data and Associated Builders and Contractors.